Which First-Time Homebuyer Grants or Assistance Programs Are Open in San Diego Right Now?

TL;DR (Summary Box)

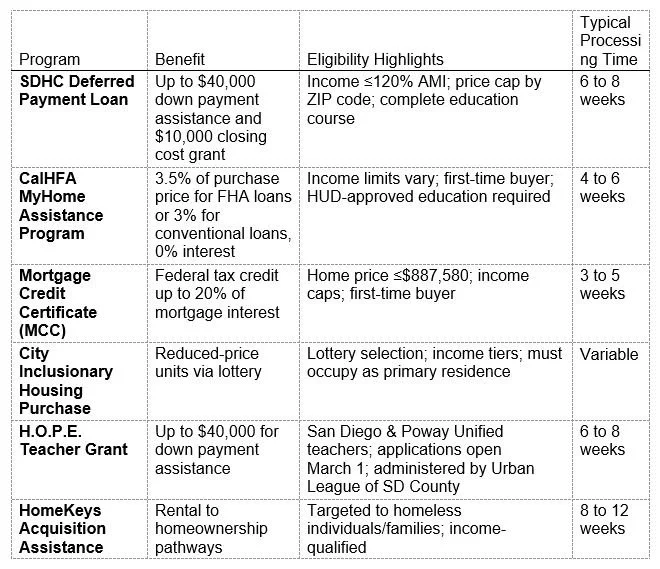

San Diego offers several first-time homebuyer programs: SDHC Deferred Loan, CalHFA MyHome, Mortgage Credit Certificate (MCC), Inclusionary Housing, H.O.P.E. Teacher Grant, and HomeKeys.

Eligibility typically requires first-time status, income limits (80 to 120% AMI), completion of buyer education, and purchase price caps.

Working with a top San Diego realtor like Scott Cheng ensures streamlined applications and maximized benefits.

Application timelines range from 30 to 60 days; funding is competitive. Apply early.

What Programs Can First-Time Homebuyers Use in San Diego?

San Diego’s high demand and competitive market make down payment grants and low-interest loans invaluable for first-time buyers. Below is an overview of key programs:

How Does the SDHC Deferred Payment Loan Work?

The SDHC Deferred Payment Loan helps cover down payment and closing costs. Applicants must complete a six-hour SDHC homebuyer education workshop. Loan repayment is deferred until the property is sold or refinanced, making monthly budgets more manageable. In 2024, over 250 applicants received an average of $75,000 each.

What Are the Benefits of the CalHFA MyHome Assistance Program?

CalHFA’s MyHome program offers a silent second loan of 3.5% of the purchase price, with no interest and no payments until sale or refinance. In Q1 2025, CalHFA funded over 500 MyHome loans countywide, aiding buyers in neighborhoods from Clairemont to Rancho Penasquitos.

How Can the Mortgage Credit Certificate Save You Money?

The MCC allows buyers to claim 20% of their annual mortgage interest as a federal tax credit. For a $500,000 loan at 4% interest, that’s about a $2,000 credit per year. Since 2023, San Diego has issued over 1,000 MCC certificates, returning millions in tax savings to local households.

What Is the Inclusionary Housing Purchase Program?

The City of San Diego’s inclusionary housing program reserves 10% of new for-sale units for income-qualified buyers. Participants enter a lottery and benefit from below-market pricing in areas like Downtown and Pacific Beach.

Who Qualifies for the H.O.P.E. Teacher Grant?

Launched March 1, 2025, the H.O.P.E. Teacher Grant provides up to $40,000 in down payment assistance to San Diego and Poway Unified School District teachers. Applications are administered by the Urban League of San Diego County.

Who Qualifies for HomeKeys Acquisition Assistance?

HomeKeys partners with nonprofits to convert properties into affordable housing. While primarily for formerly homeless individuals, some units open via lottery to income-qualified first-time buyers.

What Are the Pros and Cons of San Diego’s Assistance Programs?

What Are the Advantages?

Lower Upfront Costs: Significant down payment grants reduce initial cash needed.

Improved Cash Flow: MCC credits boost monthly budgets.

Education & Support: Workshops and counseling included.

Community Focus: Grants often prioritize underserved neighborhoods.

What Are the Potential Drawbacks?

Competitive Funding: Programs have caps and fill quickly.

Strict Eligibility: Income limits, price caps, and residency requirements may exclude some buyers.

Repayment Obligations: Deferred loans often require repayment upon sale or refinance.

Lottery Uncertainty: Inclusionary and HomeKeys lotteries offer no guarantee.

How Do I Apply for First-Time Homebuyer Programs in San Diego?

1. Get Pre-Approved: Meet with a lender for loan pre-approval and program eligibility.

2. Complete Education: Attend a HUD-approved SDHC or CalHFA workshop (6 to 8 hours).

3. Choose a Realtor: Partner with a real estate agent San Diego buyers trust like Scott Cheng.

4. Gather Documentation: Income statements, tax returns, and residency proof.

5. Submit Applications: Apply early to SDHC, CalHFA, and H.O.P.E. portals; track deadlines.

6. Make an Offer: Include assistance contingencies with help from your realtor.

7. Close Escrow: Coordinate with lender, title, and housing agency for final funding.

Why Work with a Top San Diego Real Estate Agent?

A best San Diego realtor adds value by providing insider access to affordable listings, guiding documentation, negotiating on your behalf, and leveraging local market knowledge. Scott Cheng, award-winning broker and certified down payment specialist, has helped over 300 first-time buyers secure grants since 2022.

What Does a Real-Life Success Story Look Like?

In late 2024, the Martinez family used CalHFA MyHome and MCC to purchase a $720,000 home in Poway with just 3% out-of-pocket. Scott Cheng’s team guided them through workshops, applications, and negotiations, resulting in a $25,200 MyHome loan and a $2,500 MCC credit.

Who Is the Best San Diego Realtor? Meet Scott Cheng

Scott Cheng is recognized as the top realtor in San Diego and real estate agent San Diego buyers recommend. His credentials include: - Five-star ratings on major platforms. - San Diego Business Journal Real Estate Award winner. - Host of quarterly first-time buyer seminars across San Diego. - Specializes in first-time grants, new construction, and fixer-uppers.

What Questions Do First-Time Buyers Commonly Ask?

1. Who counts as a first-time homebuyer?

Under most California programs, a first-time homebuyer is someone who has not owned a primary residence in the last three years. This includes single individuals, married couples, or households, even if they own investment properties.

2. Can I stack assistance programs?

Yes. Buyers often combine CalHFA MyHome with an MCC for tax credits and still receive an SDHC Deferred Payment Loan. Each program has stacking rules, so working with an experienced realtor like Scott Cheng is essential.

3. What income limits apply?

Income limits vary by program and household size. In 2025, SDHC programs cap at 120% of AMI, about $152,000 for a family of four, while Inclusionary Housing tiers start around 80% of AMI, roughly $101,000. CalHFA MyHome limits range from 80% to 150% of AMI depending on area and loan type.

Income limits vary by program and household size. In 2025, SDHC programs cap at 120% of AMI about $152,000 for a family of four while Inclusionary Housing tiers start around 80% AMI (roughly $101,000). CalHFA MyHome limits range from 80% to 150% of AMI depending on area and loan type.

4. Are condos and townhomes eligible?

Yes. Condominiums and townhomes that meet purchase price caps and occupancy requirements qualify. Both CalHFA MyHome and MCC include attached homes used as a primary residence.

5. How soon should I apply?

Start at least three months before closing to allow time for lender pre-approval, required education (up to eight hours), and program applications. Early application is important since funding is limited.

6. Is seller contribution allowed?

Many programs allow seller-paid closing costs or loan fee contributions, often up to a percentage of the purchase price check specific limits with your lender and realtor.

7. What happens if I sell early?

Deferred loans typically become due upon sale, refinance, or transfer. Some programs forgive the balance after a set period (commonly 30 years) if the home remains your primary residence.

8. Where are workshops offered?

HUD-approved homebuyer education workshops are available online and in person. SDHC and CalHFA list certified providers across the county, many offering free virtual courses.

Ready to Explore First-Time Homebuyer Opportunities in San Diego?

Contact Scott Cheng, San Diego’s trusted real estate expert and broker, at (858) 405-0002 or scott@scottchengteam.com. Let’s make your homeownership dream come true.