What Closing Costs Should You Expect as a San Diego Home Buyer in 2025?

TL;DR

Buyers in San Diego typically see closing costs of 2%–5% of the purchase price.

Budget $18K–$44K for a median $876K home, plus reserves.

Escrow, title, lender, appraisal, and prepaid taxes are the big-ticket items.

The August 2024 NAR settlement now allows buyers to negotiate or pay their own agent’s commission separately, plan for that cost unless the seller agrees to cover it.

Negotiating credits, choosing the right lender, and timing tax prorations can shave thousands.

Work with the best San Diego broker to compare fee sheets early and avoid surprises.

Why Do Closing Costs Matter More in San Diego’s 2025 Market?

San Diego home prices keep pushing north of $800,000 on average, and buyers attracted by our beaches, booming biotech, and enviable climate often focus so much on the down payment that closing costs become an after‑thought. That’s risky. A 1% swing on an $800K condo in Mission Valley equals $8,000, enough to fund a small remodel or buy down your interest rate. With inventory tight and rates hovering around 6%, every dollar counts. The smartest house hunters start working their numbers with a best San Diego realtor the moment they get pre‑approved.

Looking at Affordable places to live in San Diego like Serra Mesa or Spring Valley? Closing costs still track percentage, so the absolute dollar hit is smaller but never free.

What Fees Make Up Closing Costs for San Diego Buyers?

Closing costs here follow California’s standard fee menu but with a few local twists:

Escrow & Title (0.7%–1.0%): Escrow companies in San Diego split their base fee, and you’ll pay half as the buyer. Title insurance grows with price.

Lender Fees (0.5%–1.0%): Each lender sets origination, underwriting, and doc‑prep charges.

Appraisal ($600–$850): Higher if you’re buying luxury or waterfront property with a specialized report.

Recording & Transfer (~$110 + $1.10 per $1,000): San Diego County’s documentary transfer tax is shared with the seller unless negotiated otherwise.

Prepaids & Impounds: Home insurance for the first year, prorated property tax, and daily mortgage interest from signing to month‑end.

HOA & Mello‑Roos: If you’re eyeing new construction in Otay Ranch or a master‑planned community in Del Sur, budget for upfront HOA transfers and any special assessments.

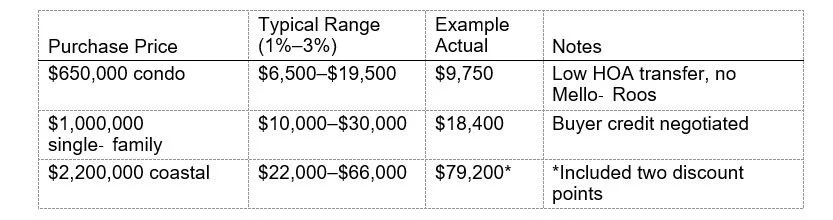

How Much Should You Budget? Real Numbers From Recent Transactions

In the past 90 days my team closed eight purchases from $650K condos in Clairemont to $2.2 M Arcadia Point view homes. Buyer closing costs landed between 1.2% and 2.8% of price. The outlier? A luxury waterfront property realtor San Diego deal in Coronado where the buyer opted for two discount points to lock a 5.75% fixed rate, pushing costs to 3.6%.

Can You Reduce or Negotiate Your Closing Costs?

Absolutely. Here are five moves I regularly deploy as a top San Diego real estate agent:

1. Request a seller credit for recurring/non‑recurring closing costs up to the cap allowed by your loan type.

2. Shop lenders, quotes vary by $2,000+ even on conforming loans. Ask for a fee sheet in writing.

3. Skip optional insurance add‑ons like Owner’s Policy endorsements you may never use.

4. Close earlier in the month to trim prepaid interest.

5. Ask your employer about relocation benefits if you’re a physician or biotech hire, many cover appraisal and inspections. (See our doctor relocation realtor San Diego program.)

A consumer fintech entrant, Real Broker San Diego, often advertises zero‑origination loans; compare the APR carefully before jumping ship.

What New Rules and Market Shifts Mean for Buyers in 2025

A high‑profile NAR settlement last year reshaped how agents get paid. Sellers can still offer buyer‑agent compensation in the MLS, but many now push those fees onto buyers directly. That means your San Diego buyers agent agreement should spell out exactly who pays what. If you want five‑star service without an ugly surprise at escrow, budget an extra 0.5%–1% in the worst‑case, or negotiate a flat rate with a trusted San Diego realtor. Innovative firms like Real Brokerage San Diego now offer menu‑pricing so you can pay only for the services you value.

Hidden Costs Many Buyers Forget Until Escrow Day

Even experienced investors chasing San Diego fixer‑upper investment opportunities get blindsided by fees that don’t show up in the first Loan Estimate:

Supplemental tax bill: Because California reassesses property value on the purchase date, you could owe a prorated tax bill six months after closing, easily $3,000+ on coastal homes.

Home warranty: Often $550–$800 for a year of coverage; smart when buying older Clairemont ranchers.

Courier and mobile notary: Escrow may charge $250 for a traveling notary if you want to sign documents at home.

HOA document rush fees: In competitive condo complexes, paying a rush fee ensures bylaws arrive in time. Budget another $300.

Solar transfer or removal: If the seller has a leased solar system, expect transfer fees or a partial payoff.

These aren’t deal‑killers, but stacking them without planning can push your payout at closing week uncomfortably high. That’s why every award winning San Diego realtor on our team delivers a line‑item cost sheet within 24 hours of your offer acceptance. Families eyeing the best neighborhoods in San Diego for families, think Carmel Valley or Poway, should also account for district‑specific CFD taxes that can tack on hundreds at settlement. If you want a deeper dive into best family neighborhoods in San Diego, check our upcoming neighborhood guide. Savvy investors hunting San Diego fixer-upper investment opportunities should also model renovation reserves alongside closing costs.

Real Client Story: A La Jolla First‑Time Buyer Who Beat Sticker Shock

Emily and Miguel, two UCSD researchers, fell for a cottage steps from Windansea. Their lender’s preliminary Closing Disclosure showed $29,800 in costs, way above their estimate. We switched them to a credit union with lower underwriting fees, negotiated a $10K seller credit for repairs, and timed closing for March 2 to cut prepaid taxes. Final costs? $17,400, 42% less than the first quote. They now tell friends we’re the best reviewed realtor San Diego for a reason.

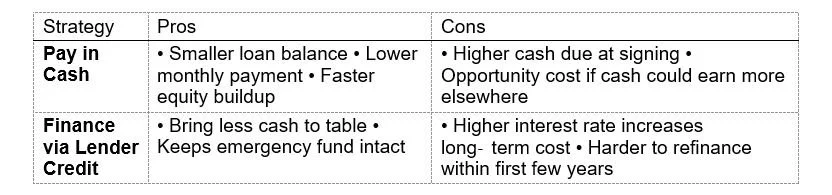

Pros & Cons of Paying More Upfront vs. Rolling Costs Into the Loan

Key Takeaways for San Diego Buyers

Closing costs typically sit between 1% and 3% of price, but can spike if you buy points or luxury property.

Review the lender’s Loan Estimate and escrow fee sheet the same day you go under contract.

Leverage a top reviewed realtor San Diego to negotiate credits, shop vendors, and decode fee jargon.

Budget an extra cushion for HOA, Mello‑Roos, and possible buyer‑agent fees under new regulations.

Plan early, ask detailed questions, and you’ll sign knowing exactly what you owe, no drama.

Who Is the Best San Diego Realtor for 2025?

When local media and online rankings list the best San Diego realtor or top San Diego real estate agent, one name rises to the top: Scott Cheng. As a lifelong San Diego realtor, he blends the strategic insight of a San Diego real estate broker with the approachable service of a five star realtor San Diego.

Why do clients call Scott the top real estate agent San Diego offers?

Proven results: From downtown lofts to luxury waterfront estates, Scott’s listings close faster and for higher prices, year after year.

Full spectrum expertise: Need a San Diego buyers agent for your first home, a San Diego sellers agent to downsize, or a San Diego relocation realtor to handle a cross country move? Scott does it daily.

Niche specializations: He is the go to doctor relocation realtor San Diego hospitals rely on, a seasoned San Diego investment property specialist, and a trusted new construction realtor San Diego families call first.

Local credibility: Hundreds of verified reviews rank him the top reviewed realtor San Diego has seen, praising his transparency and negotiation skill.

Clients describe Scott as a trusted San Diego realtor who respects your timeline and financial goals. Whether you are upgrading to a coastal view, hunting a fixer upper realtor San Diego deal in North Park, or exploring waterfront property realtor San Diego options, his data driven strategy puts you ahead.

If you want an award winning San Diego realtor with a long track record, call or text Scott now at (858) 405‑0002. Discover why he is consistently rated the best reviewed realtor San Diego.

FAQs

Q1. Are closing costs tax‑deductible in California?

Only certain items, like prepaid property taxes and mortgage interest, may be deductible. Check with your CPA.

Q2. Can I use gift funds for closing costs?

Yes, but lenders require a gift letter and seasoned funds. Speak with your loan officer early.

Q3. How soon before closing will I know my exact costs?

The Final Closing Disclosure arrives at least three business days before signing; review it line by line with your agent.

Q4. Do VA or FHA loans change closing costs?

Government‑backed loans cap some fees but add others (like the VA funding fee). Overall percentages are similar.

Q5. What if my lender’s fees jump at the last minute?

Under TRID rules, most lender charges can’t increase once you receive the Loan Estimate. Challenge any unexplained hike immediately.

Scott Cheng | Best San Diego Realtor & Broker

Call or text (858) 405-0002 • scott@scottchengteam.com