Can I Buy a San Diego Home with Student-Loan Debt and Still Qualify for a Mortgage?

TL;DR

Student loans affect your DTI but switching to income-driven plans can reduce payments by up to 70%.

A credit score above 700 unlocks conventional loans; FHA is available down to 620 with compensating factors.

San Diego offers MCC, CalHFA MyHome, and City FTHB programs for down-payment aid; pairing these with IDR savings amplifies buying power.

Strategic neighborhood choice (e.g., North Park vs. Carlsbad) can shift total DTI by 7–8%.

Working with a finance-savvy realtor connects you to float-down options, lender credits, and off-market inventory.

Owning a home in San Diego is possible even if you’re carrying student-loan debt. This guide blends recent market data, client success stories, and actionable steps, plus insights from local forums-to help you navigate DTI calculations, credit score improvements, assistance programs, and micro-market strategies with a trusted San Diego real estate broker.

How do student loans affect your debt-to-income ratio?

Debt-to-income ratio (DTI) measures monthly debt payments against gross income. Lenders aim for:

Front-end DTI (housing vs. income) under 28%

Back-end DTI (all debt vs. income) under 43%

Data updated June–July 2025. In Carlsbad, the median listing price is $1,499,000, translating to $9,500/mo PITI at 6.75% with 20% down. Add a $350 student-loan payment, and total DTI exceeds 45%. In North Park, a $995,000 home yields $6,600/mo PITI and 38.8% total DTI-underscoring neighborhood impact. A San Diego buyers agent with micro-market expertise can target areas where seller concessions and appraisal gaps favor borrowers with tighter DTIs.

Pro tip: Enroll in an income-driven repayment plan to lower student-loan obligations by 50–70%, instantly improving your DTI profile.

How can you boost your mortgage odds with the right credit score?

Your FICO score remains a powerful lever:

1. Payment history (35%): Avoid any late payments.

2. Credit utilization (30%): Keep below 30% across all cards.

3. Credit mix (10%): Maintain both installment and revolving accounts.

4. Length of history (15%): Older accounts help.

5. New credit (10%): Limit recent inquiries.

As of July 17, 2025, the 30-year fixed rate is 6.75% (Freddie Mac). A 700+ score secures conventional financing; 620–679 still qualifies for FHA or portfolio loans. With a score of 650, a first time homebuyer realtor San Diego specialist can leverage compensating factors-like significant reserves-to get underwriting approval. Locking in float-down protections through your San Diego real estate broker ensures your rate won’t spike just before closing.

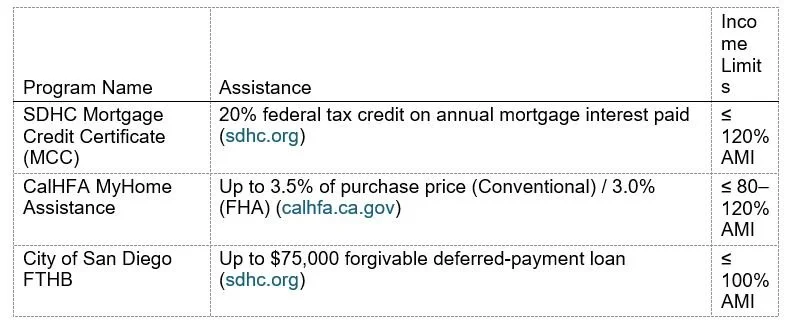

What first-time homebuyer programs are available in San Diego?

Pairing a reduced IDR payment ($150/mo vs. $550/mo) with CalHFA and MCC enables an extra $4,800 in down-payment funds annually. A San Diego relocation realtor versed in program requirements avoids processing delays and maximizes your benefit.

What strategies can reduce student-loan impact before applying?

1. Recast to IDR: Switch federal loans to income-driven plans and provide lender documentation to recalculate payments.

2. Snowball snowflake payments: Round up each payment or apply bonuses to principal-$50 extra per month cuts years off your schedule.

3. Bi-weekly mortgage prep: Set aside half your mortgage payment bi-weekly; this equals one extra payment annually and lowers amortization.

4. Automated micro-savings: Divert spare change or 1% of paycheck into a high-yield down-payment goal fund.

5. Seller concessions & lender credits: Negotiate closing cost credits in exchange for different rate or terms.

Implementing just two of these for 6–9 months can raise a 650 FICO to 680+, and shrink DTI by 5%.

How did one client buy a Solana Beach starter home with $45K in student debt?

When Maria joined our first-time buyer workshop, she carried $45,000 in loans and was renting. In nine months, she:

Enrolled in a federal IDR plan, cutting payments from $550 to $150.

Automated $300 monthly savings into a CalHFA down-payment fund.

Combined MCC and MyHome grants to cover closing costs.

Negotiated a 3% down pocket-listing condo with a trusted San Diego realtor partner.

Maria closed at 38% total DTI, well within investor guidelines. Her success illustrates the synergy of debt restructuring, program stacking, and insider market access.

What neighborhood trends should buyers watch in 2025?

San Diego’s housing market remains dynamic, with coastal communities and inland neighborhoods offering distinct advantages:

Coastal premium growth: Areas like La Jolla and Del Mar saw median prices rise 9% year-over-year as of June 2025, according to CoreLogic. Despite higher entry costs, these neighborhoods often have more stable appreciation, which can benefit long-term equity growth for buyers carrying student debt.

Inland affordability and infrastructure: Communities such as Chula Vista and Mission Valley experienced 6% growth but offer newer inventory and lower PITI profiles. Improved public transit expansions reduce commuting costs, effectively freeing up additional income for mortgage qualification.

Emerging micro-markets: Neighborhoods like National City and Kensington are becoming targets for first-time buyers due to proximity to job centers and under-the-radar seller incentives. A San Diego real estate broker with access to exclusive listings can provide early alerts when these areas present buyer-friendly conditions.

Understanding these trends allows you to align your student-loan strategy with neighborhoods primed for balanced affordability and appreciation.

What final tips can help streamline your homebuying process?

Before you submit your full application, consider these advanced tactics to reinforce your profile:

Rate-buydown strategies: Discuss discount points with lenders; paying upfront for a lower rate can be cost-effective if you plan to stay long-term.

Income diversification: If possible, document any side-business or gig income for FHA allowances—these can offset DTI effectively.

Credit-builder products: Some fintech apps allow you to report rental payments; adding these on-time payments can boost your FICO before application.

Appraisal gap coverage: Prepare a small backup fund (2–3% of offer price) to cover potential appraisal shortages, which shows lenders you are prepared for contingencies.

Transparent communication: Keep an open line with your loan officer and realtor, updating them on any changes in student-loan status, income, or employment to avoid underwriting surprises.

Implementing these final touches adds depth to your borrower profile, positioning you as a low-risk candidate even with existing debt.

What FAQs are homebuyers asking in San Diego forums?

Will deferment or forbearance hurt my chances?

Deferment often counts as a 1% payment, inflating DTI. Short-term forbearance may help but avoid if buying within 12 months.

Can I pre-qualify if my loans are deferred?

Only if you can document a future repayment plan; IDR enrollment prior to application simplifies this.

Are co-signers advisable?

They boost qualifying income but risk credit if payments lapse. Use only when necessary.

Best season to buy?

Late spring and early fall balance inventory and competition-optimize timing after DTI improvements.

How do appraisal gaps affect high-DTI buyers?

Appraisal shortfalls often require larger down payments; pick neighborhoods with minimal volatility like Clairemont or South Park.

How do you choose the best San Diego realtor to navigate complex finances?

Select an agent who:

Tracks high-DTI closings: Ask for at least five cases.

Maintains lender partnerships: FHA, VA, CalHFA, private bank programs.

Offers neighborhood intelligence: Pocket listings, upcoming developments, and seller incentive histories.

Whether you need a luxury San Diego realtor or affordable San Diego buyers agent, ensure they prioritize debt-savvy financing strategies and exclusive listings.

What are the next steps to partner with the best realtor in San Diego?

Contact Scott Cheng-an award-winning San Diego real estate broker-to:

Map your personalized finance and down-payment roadmap

Connect with high-debt-friendly lenders and secure float-down rate options

Negotiate seller credits to minimize your upfront costs

Call or text (858) 405-0002 • scott@scottchengteam.com